Affiliate Disclosure: When you click links at Only Greats & make a purchase, we may earn a commission. As a free site, we join affiliates like eBay & Amazon to help offset our costs. THANK YOU for your support!

Last Updated On: September 11th, 2023

So you finally thought it would be a good idea to buy sports card insurance for your sports cards and memorabilia collection.

Most collectors reach this point when they amass a collection of baseball cards or autographed memorabilia that has accumulated in value and deserves more serious attention in case of a disaster.

Table of Contents

For me, the decision to get sports card insurance hit me when a friend of mine shared a 10 second video of her apartment building gushing water from a bursted pipe in the stairwell right outside her front door. It read:

“I need to move in the next 3 days, my building just flooded.”

I shot an email to my insurance agent the very next morning to learn about the insurance options available to me, as my collection had soared to over $50,000 of value in recent years. I discovered pretty quickly that renters insurance wasn’t going to cut it (more on this later).

The sports cards industry is considered very volatile. Prices swing in major directions, and lately it seems prices can’t stop going up (and rising still). Nothing illustrates this better than one of my Jordan rookies having jumped from $600 to $3500 in just 3 years (almost 6x in value!).

So if renters insurance isn’t a good fit for sports cards, how about homeowners insurance?

Let’s go over some of the primary ways to insure your sports cards.

Sports Card Insurance Summary TL;DR

| Insurance Option | Recommended for Sports Cards? | Cost of Insurance | Notes |

|---|---|---|---|

| Renters Insurance | No | N/A | |

| Homeowners Insurance | No | N/A | |

| Separate Policy Amended | Yes | Varies widely, very costly | cumbersome and requires appraisals |

| CIS Insurance Company | Yes | $342 per $50,000 value annually | Good for collectibles stored at home, storage, or at a bank |

| American Collectors Insurance | Yes | $300 per $50,000 value annually | Good for collectibles stored at home, storage, or at a bank |

| PWCC Vault | Yes, best option | 1% intake fee, .5% 1st year. $750 per $50,000 value 1st year | More expensive, but stored at PWCC, many more benefits (read below) |

Renters & Homeowners Insurance Won’t Help

Renters and homeowners insurance policies are very similar when it comes to protecting your personal property. As a renter, you usually carry a renters insurance policy (sometimes mandated by your landlord). Similarly, as a homeowner you carry a homeowners insurance policy (sometimes mandated by your mortgage loan company).

Standard policies have specified caps, or limitations set on how much you can claim for a given type of loss (e.g. jewelry, electronics, computers, etc.).

The limits can be adjusted for your specific needs. If you have $15,000 in jewelry, your insurance agent can boost your policy from a maximum of $1000, to a coverage of $15,000 for additional “premium” cost to you (i.e. a more expensive policy).

When it comes to sports cards, this is where these policies become borderline useless. In my homeowners insurance policy with Geico, it states the following items as ineligible for replacement cost.

“Memorabilia, souvenirs, collectors items and similar articles, whose age or history contribute to their value.”

Since baseball cards typically go up in value as they age, then insurance will only cover the “cash value” of what you paid for them (assuming you have receipts), not their actual value as it increases over time (what would qualify as “replacement cost”).

The insurance company is happy to insure for “replacement cost” on most things otherwise. If your fridge is insured and worth $1000 today, in 2 years it will depreciate to $650. If it completely breaks down and you make a claim in 2 years, the insurance company can simply pay to fix your current fridge, or buy you a replacement at $650 (current market price) to meet the terms of the policy.

So if your collectibles were purchased for $10,000 in 2016, and they’re worth $17,000 in 2020, the renters or homeowners insurance would only cover up to $10,000 (assuming you had your limits raised as mentioned in the jewelry example above).

Obtaining an Amended Insurance Policy for Sports Cards

After discovering how silly it would be to depend on my standard renters or homeowners insurance policy to cover my sports cards, I reached out to a State Farm Insurance agent to learn whether they provided any alternative solution for sports card insurance.

Long story short, they were happy to write a policy for my sports cards and collectibles, however I needed to have them formally appraised to determine their actual value to be covered. This initially sounded like it might work. I could use eBay to determine the real market value of my cards and simply share the results with my agent, right?

No.

Apparently the “underwriters” prohibited eBay as a valid method for appraising the value of my sports cards. What? Why? And what is an underwriter anyway? All questions I asked the State Farm agent.

The underwriters determine what constitutes a valid way to value your personal property, and eBay was not one of the approved ways. I contended if I could literally post a basketball card on eBay for auction, and get tens, if not hundreds of bidders to confirm the value of my card in an auction-style format, this is exactly the current market for my card. The stock market works exactly this way!

Needless to say, I didn’t pursue the battle very hard from here.

The thought of appraising my cards through an actual appraiser made zero sense. It would cost too much time and money to get a formal appraisal, only to consider it outdated and beneath the market value for my sports cards in a few months or a year later. I would have to continuously get new appraisals for all my cards just to cover the value as it increased over time.

Sports Card Insurance Companies

While standard insurance companies require jumping through hoops to insure your collectibles, there are insurance companies that specialize in sports card insurance in particular. They understand the nature of collecting, and the convenience of designing insurance policies that are reasonable, flexible, and convenient for customers.

Collectibles Insurance Services

One of the longest standing collectibles insurance companies around is aptly named Collectibles Insurance Services, and was founded way back in 1966.

They’re also the #1 google search result for “collectibles insurance” as of July 2020.

Using their online quote system, you can get a quick understanding of what it would cost annually to insure your collection. For example, a collection valued at $50,000 was quoted at $342 in annual premium cost. That’s not bad — works out to just a little over half of 1% of the total value of your collection per year.

Keep in mind you can even qualify for discounts if your collection is stored in a safe, or stored at home where you have an alarm system, or even if you have it stored at a bank (i.e. safe deposit box). Note: the quote above did not include any of these discount options.

Another neat option of CIS is that they offer an “automatic monthly increase” where your total insurance value can be increased each month by 1% to account for appreciation or additional cards added to your collection.

For example, if you insure a collection at $10,000 today, in a month your insurance policy will be covered for up to $10,100 (1% increase in a month), and your premium cost adjusted accordingly for the extra $100 of insurance. Compare this with the home or renters insurance policies we already discussed, and it’s easy to see how the automatic option is so much more convenient than needing to get new appraisals completed constantly.

One minor drawback is that you will still need to itemize and appraise any collectibles or card sets valued at $25,000 or more. For most collectors, this shouldn’t be a huge deal unless you have a few 1952 Mantles laying around 🙂

CIS also insures stamps, coins, comics, art, and many other types of collectibles if you’re into that sort of thing.

I can’t speak to the overall quality of their service, nor vouch for them. Please do your homework.

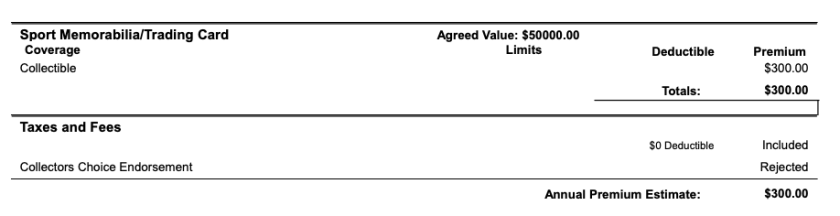

American Collectors Insurance

Another comparable insurer in the collectibles space is American Collectors Insurance. They have a more updated, reputable site, and also tout their 4,000+ Trustpilot reviews front and center.

In regards to primary features, they, too, increase your policy with what they call “Inflation Guard”. In particular, ACI’s website states “Your policy limit will appreciate by 2% each quarter, up to 8% annually, for all items in your collection valued at greater than $2,000.”

American Collectors quote is also slightly more affordable than CIS. A $50,000 collection was estimated at $300 annually with $0 deductible to insure. You can reduce the cost to just $285 with a $500 deductible (i.e. if you ever make a successful claim, you’ll receive $500 less on any reimbursement amount).

In addition to their sports cards and memorabilia insurance, ACI primarily insures collectible cars, trucks, motorcycles, and other similar exotic collectibles.

As with CIS, I can’t speak to the overall quality of American Collectors’ service, nor vouch for them. Please do your homework before choosing the right insurance provider for your valuables.

A Modern Way to Insure: PWCC Vault Account

One of my favorite new services is the PWCC Vault operated by PWCC. It launched around 2019, and solves a lot of the pain points of sports card storage, insurance, and also providing liquidity with flexible buying and selling.

First things first, PWCC is a leader in sports cards auctions, and particularly consignment of auctions on eBay. You can ship your collectibles straight to PWCC to auction them off on eBay. They take care of everything from writing a compelling marketing description of your card(s), take beautiful high-resolution pictures, and post them to eBay so you don’t have to. They also collect a reasonable fee for their work — sometimes even less than eBay charges in listing fees, especially when you tack on what PayPal also takes from you (e.g. 2.99% transaction fee for Goods and Services).

Back to the Vault service. When you sign-up for a vault account, you’re assigned a unique shipping address straight to the vault located in Oregon in the United States. There, your cards are stored, and high resolution scans of the front and back are provided upon intake.

Once your vault portfolio is digitized to an online portfolio, you’ll see the value assigned to each card, which also corresponds to the insurance amount provided by PWCC.

PWCC charges a 1% intake fee for most of your graded cards, and then .5% in the first year. Generally speaking, if you sent $10,000 worth of cards into your PWCC Vault account, you’d pay $100 for intake fees upfront, and then another $50 for the first year of storage/insurance, billed monthly. Future years are just .25% storage/insurance cost, so it’ll just be $25 per $10,000 in value, per year.

On the surface, this is a little more costly than the collectibles insurance providers mentioned earlier in this post, but when you factor in the future years’ costs at just .25%, and also the flexibility you get when buying and selling cards on the PWCC marketplace with the click of a button, it really blows the other options out of the water.

I couldn’t vouch for the collectibles insurance providers as I have never used them, but I do personally use the PWCC vault and highly recommend it! I have bought and sold via PWCC countless times, and the benefits of having the flexibility and liquidity in my collection without needing to receive shipments at home, store, insure, and post items online for sale, I can’t think of a better value for the cost.

One other major benefit worth noting: given the vault is located in a tax free state like Oregon, your online purchases shipped directly to the vault do not get charged a sales tax. Imagine that’s another 5-10% in state tax savings. Nothing to sneeze at.

Protection via Separation of Sports Cards

Before I purchased insurance for my collectibles, or shifted to a PWCC vault account, I actually diversified where I stored my cards almost naturally. The concept of protection via separation is the last topic of this article, as it is likely how many of you already store your cards even without insurance policies in place.

I had old sealed wax boxes from 1981 stored in a locked storage room outside of my apartment near the garage. I still have a ton of cards in my closet in top loaders and storage boxes, some valuable and others not. I even had some stored in a fire-proof safe. The point is, the sheer separation of your cards away from the same place is a form of a poor man’s protection, but protection nonetheless. This way, any theft, fire, water damage, or otherwise unanticipated issue doesn’t impact your entire collection because it sits stored in one place.

You also may be considering a safety deposit box at your local bank. This is also a great option for storing some of your valuables away from others, but keep in mind most banks do not insure the contents of your safety deposit box. It’s definitely more secure than your bedroom nonetheless given it’s in a locked bank, behind additional secured doors with limited access, and cameras everywhere.